Read The Rest of Market Outlook’s Content Here

.elementor-widget-text-editor.elementor-drop-cap-view-stacked .elementor-drop-cap{background-color:#69727d;color:#fff}.elementor-widget-text-editor.elementor-drop-cap-view-framed .elementor-drop-cap{color:#69727d;border:3px solid;background-color:transparent}.elementor-widget-text-editor:not(.elementor-drop-cap-view-default) .elementor-drop-cap{margin-top:8px}.elementor-widget-text-editor:not(.elementor-drop-cap-view-default) .elementor-drop-cap-letter{width:1em;height:1em}.elementor-widget-text-editor .elementor-drop-cap{float:left;text-align:center;line-height:1;font-size:50px}.elementor-widget-text-editor .elementor-drop-cap-letter{display:inline-block}

Weekly Market Outlook

By Donn Goodman

January 31, 2023

We welcome you to another weekly Market Outlook. Thanks for being here.

This past week’s economic data pushed stocks into unchartered territory. First, the 4th quarter GDP came out above consensus at a blistering 3.3% pace. (It recorded 2.9% for full-year GDP). PCE (Personal Consumption Expenditures) came in as expected, but year over year was at 2.9%. Below the expected 3%.

However, digging deeper into the recently released much stronger-than-expected Q4 GDP report, you’ll find a bonus in the core PCE Deflator data. The PCE Deflator rose at an annualized rate of 2.0%. By this measure, the Fed’s 2% inflation target has been achieved—for the second quarter in a row. See chart below.

.elementor-widget-image{text-align:center}.elementor-widget-image a{display:inline-block}.elementor-widget-image a img[src$=”.svg”]{width:48px}.elementor-widget-image img{vertical-align:middle;display:inline-block}

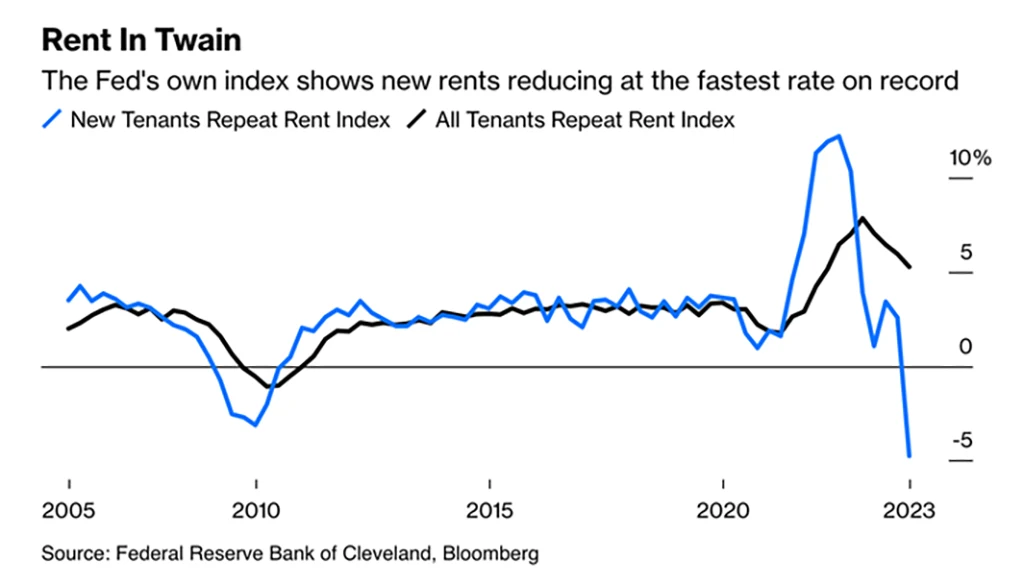

One of the bright spots of the recent economic reports, including the CPI and PCE, is that sky-high rents have come down at a brisk pace. See rent chart below:

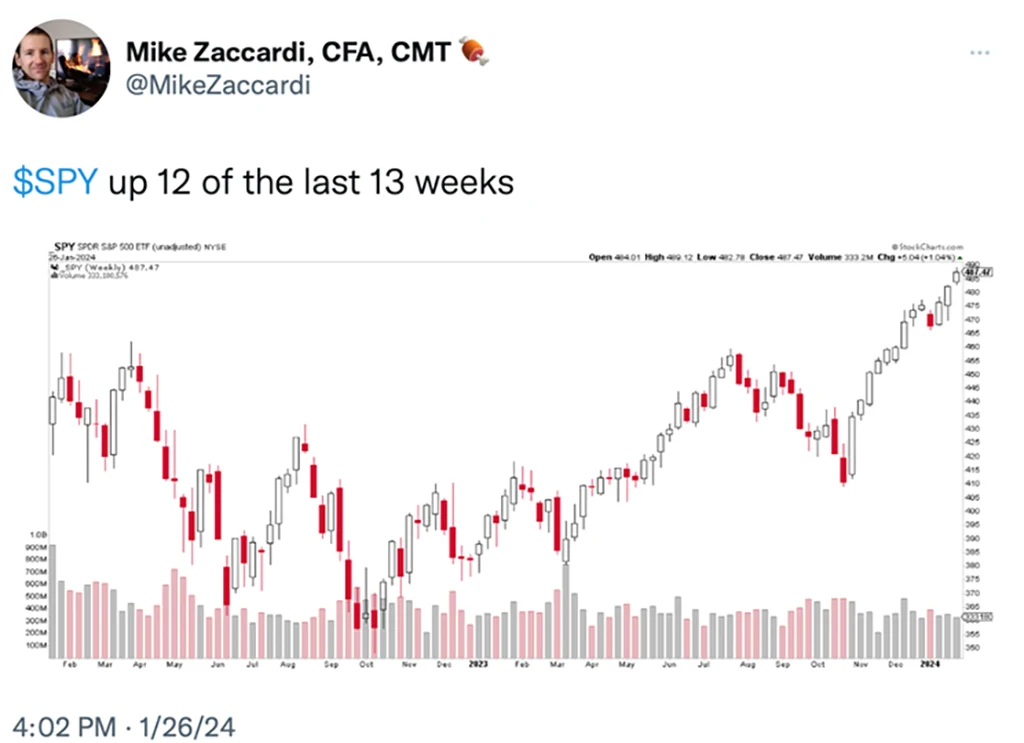

This harkens back to the beginning of November. The economic numbers then also came out showing favorable inflation cooling. You will recall that the Federal Reserve pivoted off their hawkish sentiment, and immediately, the market rocketed higher. The S&P has been up 12 of the past 13 weeks. See chart below:

Looking back to the beginning of 2024.

It seems like yesterday when we were welcoming in the New Year and beginning the process of prognosticating what might occur in 2024. Surprisingly, the markets started off weak for the first week of the New Year. But since then, it has been moving up almost daily.

So far in January, the S&P 500 (SPY) is up 2.55%, which would be annualized at 33.2%. The NASDAQ 100 (QQQ) is up 3.49%, which would be annualized at 44.5%, the Dow Jones Industrial Average (DIA) is up 1.12%, which is an annualized rate of 14.6%, and the Russell 2000 Small-Cap Index (IWM) is down -2.36% which would be an annualized rate of -30.74.

Take note of two important facts about the performance numbers above. If the positive markets (SPY & QQQ) were to continue at this pace, the 2024 returns would surpass last year for the S&P 500 and come close to matching the NASDAQ 100 for all of last year. Secondly, the more undervalued areas of the market (including small and mid-cap stocks that typically have faster growing companies), would be negative on the year.

This is likely NOT going to happen and one should not use the January returns as an indication of what will occur for the remainder of the year. (please go back to the early 2024 Market Outlooks and read what historically happens for a better perspective)

If you are a follower of MarketGauge and get a chance to join Keith, Mish, or Geoff’s coaching sessions and webinars, you are aware that the January “Calendar Range,” which was completed on January 16th, can set the tone and define inflection points for the rest of the year. For more information on the January Calendar Range see Mish and Geoff’s recent video for StockCharts.

As we noted last week, it was no surprise that the first week of the year showed market weakness, given the positive and robust October and November with outsized gains. Investors wanted to take some profits but were waiting to push those off until the 2025 income tax period.

If you have not had a chance yet to read last week’s Market Outlook, you can click here to be taken to that article.

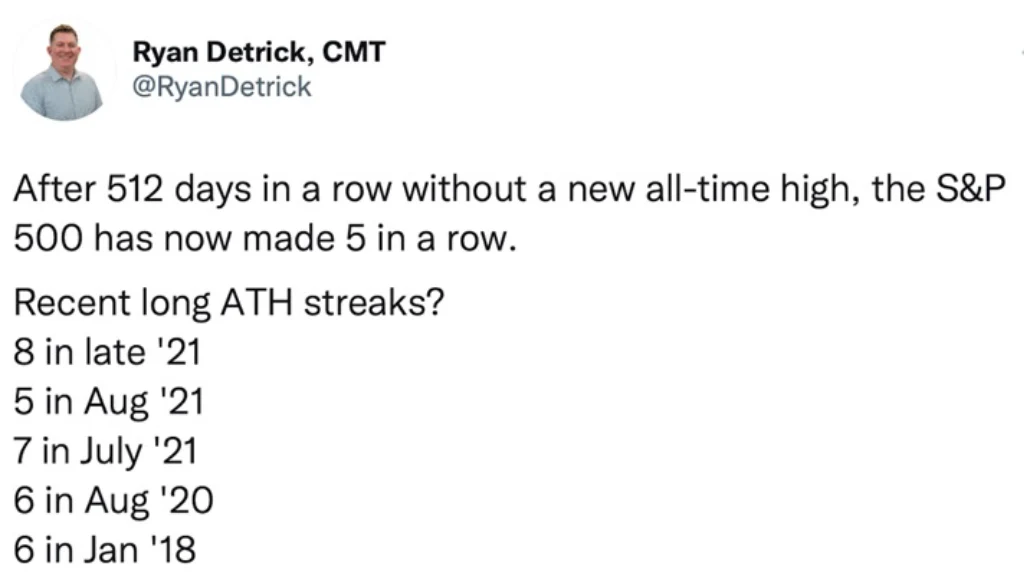

Looking at New All-Time Highs in the S&P 500

The S&P 500 also closed at record all-time highs (ATH) for the 6th consecutive day on Thursday, making this the longest streak of record highs since November 2021.

Regarding the record new ATH of the S&P 500 Wednesday evening, Ryan Detrick of the Carson Group pointed out how rare these truly are. See his commentary below:

We have provided a history below of how many ATH have been recorded each year looking back to 1929. Please note the many years with 0 (zero) new All Time Highs and other periods where we many successive years with no new ATH for a considerable and extended period of time.

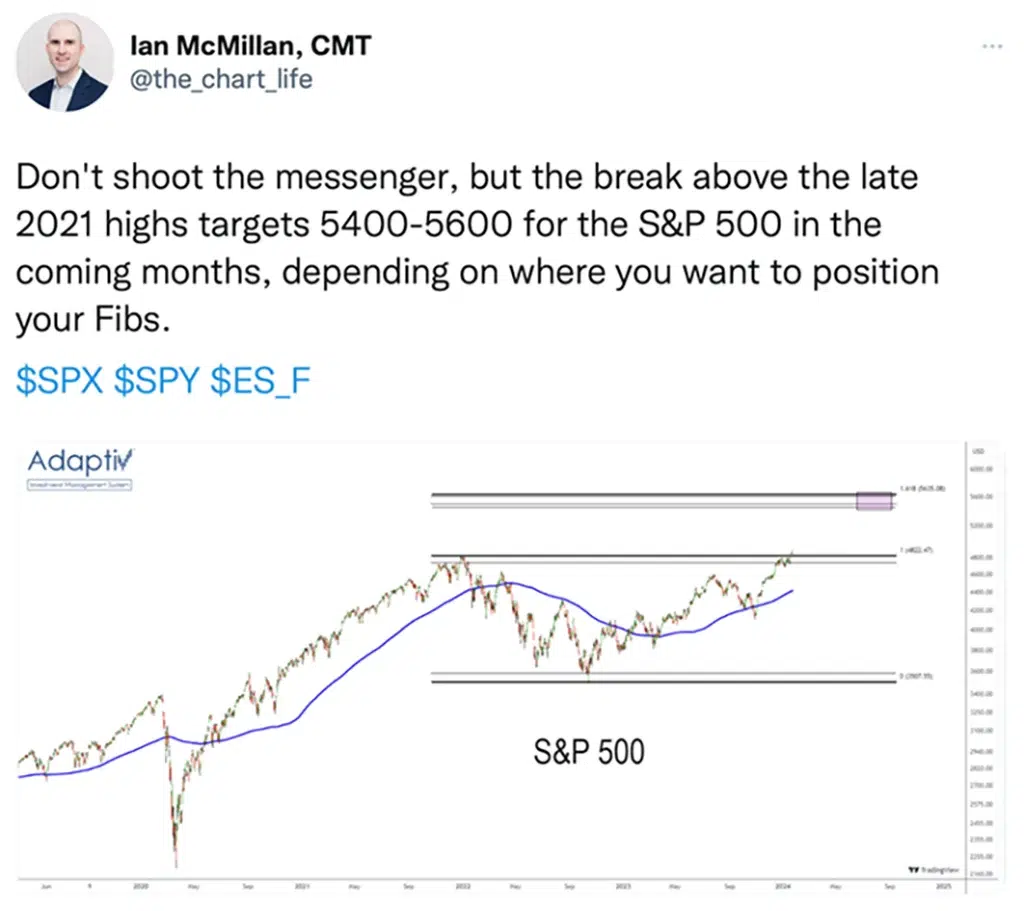

When price is in uncharted territory like this, technicians and analysts often use Fibonacci extensions to establish potential resistance levels or targets.

Analyst Ian McMillan points out that the 161.8% extension of the 2022 decline is between 5,400 and 5,600 which is a move of 10% higher from here. The question is “will it move in a straight line”? To which Ian answered, “I highly doubt it, but it is a target nonetheless.” See chart below:

A look at few of the key sectors that are driving the capitalization weighted indices:

Technology. The Technology sector, with its many mega caps stocks, continues the impressive move higher. Recently, as the chart below shows, technology became a 30% weighting of the S&P 500 Index. The last time we saw this was in 2000. That was about the time when the sharp correction in Tech stocks began and lasted until 2022. Technology’s influence on the S&P 500 performance cannot be underestimated.

Within the technology sector, semiconductor stocks are also on a blistering growth phase and have entered unchartered territory.

Use the link below to continue reading about:

- The influence of the semiconductor sector on the economy

- The strength of the financial sectors

- The Magnificent 7 drops to 6

- The weekly BigView bullets

- Keith’s weekly BigView video analysis

Click Here To Continue Reading

The market’s price action and news flow can be confusing and intimidating, but investing in this environment doesn’t have to be. If you would like personal guidance and hands-on management of your assets with the assistance of tactical, risk-managed, strategies, please contact me at [email protected] or Keith at [email protected].

The post Unchartered Territory And Then There Were 6! appeared first on Southern Boating.

{kind=link}